Hi friends,

In Part 1, I discussed why the renting market is so horrendous, especially if you’re moving into the city from a more relaxed market. I highly recommend reading it if you’re an incoming grad student or someone looking to move to Boston/Cambridge.

Now I’ll talk about the buying side of the market: why I decided to buy, what the housing market is like, how the finances shape up, and the general timeline.

Decisions, Decisions

Now, why did I decide to buy rather than continue renting?

Allow me to be completely candid: I decided to buy because my dad volunteered to finance it. My father is providing the down-payment for the condo. (I’m responsible for all the mortgage payments once we close, but this would not be possible without his generosity.) It was originally his idea. He watched me struggle to figure out the renting market when I first arrived and he offered to help me buy something so I could leave the market and not have to worry about moving every other year or so. I would never have asked him to do that or even thought about it as a viable option because grad students are, you know, living right on that poverty line. But since he offered….it’s rude to refuse gifts in most cultures, you know.

The biggest reason I decided to pursue the idea and take my dad up on it, though, is that the money I pay for rent disappears. I will never see that money again. I don’t get it back when I move out (with the exception of a my fraction of the security deposit). It feels like money wasted.

With a mortgage, though, money comes back around eventually (if you’re lucky). You sacrifice a chunk of money for the down-payment and closing costs up front, and then you make monthly mortgage payments (which is mostly analogous to rent, but includes property taxes and maybe condo association fees). However, when you sell your house/condo you can recuperate all that money you put into buying and owning the place (if you’re lucky) and maybe a decent margin of profit (if you’re really lucky).

And lastly, even though I despise the establishment that is the credit report, I recognize its pervasiveness in the US economy and that it is unlikely to be replaced by a more intelligent and less faulty system. Because I don’t see myself owning credit cards in the future for the same reasons I’ve avoided them in the past and the present, having a mortgage will build credit.

Payment history is 35% of your credit report. Until recently, I was under the false assumption that paying utility bills and rent contributed to my credit score. I made sure to pay every single rent and utility bill on time. Even though I didn’t have credit cards to pay off, my other bills would show I’m reliable, right? Heh, wrong!

Not paying those small types of bills can hurt your credit score (because of accruing debt), but paying them doesn’t help. It seems like only bank-based bills (credit cards, mortgages, car loans, etc.) are counted both positively and negatively towards your credit report. Therefore, having a mortgage will help me build a stronger credit report whether I have credit cards or not. I highly doubt my dad would co-sign a second house for me – having this credit so I can stand on my own two feet for my next mortgage or car loan or whatever is immeasurably useful.

So, these are the reasons I’m making this commitment.

Understanding the Market

The market is smaller, about 63% rental market to 37% ownership according to the 2015 Boston census. Strictly based on numbers it’s more cut-throat than the renting market is. In 2015, the average cost of a house (not a condo) shot up to $1.33 million, which was a 5.9% increase from 2014 and a 55% increase from 2010. Similarly, the average price for a condo in Cambridge was $675,000 in 2015, a 47% increase from 2010 (Source).

I’m going to dispel any notions you have about negotiating down in the Boston market: Only in extremely rare cases do houses sell for less than the listed price. On average, houses/condos in Somerville sell for a 10% mark-up from the listing price. I was told that in order to be a competitive offer in this market, I should expect to offer at least a 7% markup on any place I bid on. I’ve also heard stories of places that were bought 20% above listing price. It’s really insane.

Next, you might remember from Part 1 that houses in Cambridge and Somerville tend to look like this:

Just as these houses are divided into 2 or 3 apartments (one on each floor), they can be and are often similarly divided into 2 or 3 condos. Mid-rise and high-rise condos are just as sparse as mid-/high-rise apartments. (I talked about the reasons why in Part 1.) There are pros and cons with both types (the houses and the mid-rises), and I’ll leave google to answer those questions if you really want to know.

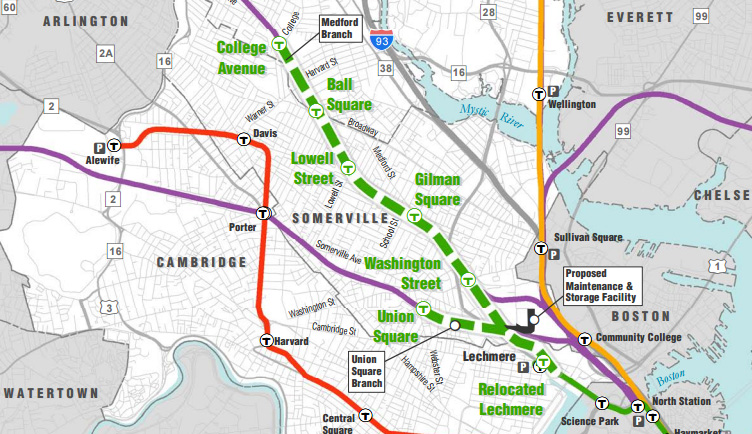

There are a lot of factors that determine the actual price of a place (e.g. laundry included in the unit/building, off-street parking), but I’d say one of the biggest determinants is proximity to a T line. For those that don’t know, Boston’s public transport is called the MBTA. They operate buses, subterranean trains (called the T), and commuter rails for those commuting from outside the city.

Just to show you the influence of the T, let’s talk a bit about Somerville. Back in the day (like, before the 1980s), Somerville used to be known as Slummerville. It was the bad neighborhood to be in. (You know the movies The Departed or Black Mass? The gangs were based off the real life Winter Hills Gang, where Winter Hills is a neighborhood in Somerville.) Part of that was because the red T stopped at Harvard Square and didn’t extend up to Davis Square. This made Somerville an isolated neighborhood from the rest of the Boston neighborhoods.

However, the powers that be decided to extend the Red Line to Davis Square in 1977, and it was actually finished in 1984. Due to the recession, the immediate growth Somerville was hoping to see didn’t happen. The number of stores decreased from 68 in 1977 to 56 in 1987. (Source: Wikipedia) However, the double whammy of the dot com bubble and the end of rent-control in the area helped Somerville really take off in the 1990s. The value of residential properties quadrupled from 1991 to 2003 (Source).

Now, as you may or may not have been able to see from the map, there’s a new isolated section: mid-Somerville. You have the red line moving up on the left and you have the orange traversing the far right side of Somerville, but the green line stops just as it reaches the border of mid-Somerville at Lechmere. The neighborhoods in the middle (Winter Hill, Central Hill, Prospect Hill, all the other hills) have suffered a bit from their lack of a direct connection to the T. For students and others that are just barely making ends meet, these neighborhoods have been refuges. The lack of T access means that rent is lower than in other neighborhoods. Recently though, the powers that be have once again put a plan into action: the Green Line Extension (GLX).

According to this article, people are already planning to develop 5,500 new condos and apartments along the GLX over the next few decades, and current residences in the vicinity of the GLX can expect a 16-25% boost in property values. Rent is expected to spike about 67% percent in the coming years, thanks to the GLX. The GLX will take Somerville from having 15% of residents within a half-mile of the T to 85% (Source).

The article also talks about the massive amounts of commercial enterprise the T will help foster. Agents and residents I’ve talked to over the past few months say that they are already experiencing increasing values and prices around the Union Square area simply because of the anticipation and promise of a T connection (sometime around 2018, they think).

[Of course, after I’ve done research and written these paragraphs I find this article: How the T has shaped and will shape West Somerville. Figures.]

In summary, the market and property values are heavily shaped by the supply/demand economics and proximity to the T.

A Method to the Madness

Alright, let’s talk about what it takes to actually buy a house/condo.

The first thing I did was find an agent. For renting, I believe you can get by just fine without using an agent. My current roomies and I used one because we were super late to the market and needed the help. For buying, though: get an agent. Especially if you’re a first-time homeowner.

In my blogs, I normally avoid saying names (there have been exceptions, like George). I don’t want to accidentally get people in trouble or cause drama, so I leave the majority of the people in my stories anonymous. However, I’m going to make another exception. My agent is Bob O’Reilly at Coldwell Bankers.

Bob has been an invaluable resource. He taught me about the market. He taught me how to spot things that make a house incredibly unattractive. One of the first homes we went to see had issues: the majority of the wood on the front deck was rotting and would cost about $15,000 to rebuild, and there was evidence of water leaking into the basement. I wouldn’t have noticed that. In another house we went to, Bob pointed out all the mold, the reason why ripping the crappy 80s wallpaper off would most likely result in yanking everything but the wood down, why that awkward, space-hogging chimney couldn’t be removed (exhaust vent for old water heater and furnace), and so many other things. In addition to him sending me listings, I sent him listings, too. When I sent listings and asked if they’d be worth seeing, he’d point out if the images had been doctored to make the rooms seem bigger or less run down, or comment on whether it was marked too high for the area. He helped me understand the financing process, why certain fees existed and what they paid for, the history and probable future of the neighborhoods we were visiting, the politics of the bidding war process, and the nature of the realty community in Cambridge. You know me, I ask a lot of questions, and Bob had been in the market for about 25 years and knew a lot of the answers.

And most importantly: when he wanted to go over things or discuss a house we just saw, he took me to a coffee shop and bought me coffee.

I swear, I would have been completely and utterly lost without his help. Bob earned his commission fee in my opinion and I would definitely recommend him to others.

One for the Money, Two for the Dough, Three for the Green

After you find an agent, the next step will be to find a mortgage loan officer. You won’t actually set up the mortgage at this point – how could you, you haven’t found a home yet – but you do want to find out what you’re pre-approved for. The mortgage loan officer, in my case a dude called Austin from Guaranteed Rate, collected a lot of info from my dad and me (tax returns, bank statements, recent paychecks, w2s, credit reports, etc.). Based on our combined financial status (like 95% Dad, 5% Me), Austin calculated our pre-approval numbers. This is a range of loan amounts that we would likely be approved once we put in for the official mortgage.

Jumping forward a bit in the timeline to a point where you’ve made an offer on a house and the sellers have accepted it, you need to hire an attorney to handle all the paperwork. (Depending on which state you live in, you might not need to have an attorney, but in MA you do.) At that point, you’re essentially paying the lawyer and their team to make sure that the bank is protected during the process. Awesome, right?

At the end of the day, you’ve got three people on payroll: your agent, who is helps you find a place and makes sure you submit things on time once your offer is accepted; the mortgage officer, who will soon know everything there is to know about you, down to whether you still owe your elementary school $3.45 in lunch money; and your lawyer, who you won’t actually meet until they sit you down in front of the Mt. Everest of paperwork with a week’s supply of pens.

Sounds fun, right?

Shop ‘Till You Drop

Once you have the pre-approval numbers from the mortgage officer, you can start narrowing down the price range of houses you’re looking at. And now it’s shopping time! My dad passed on some wisdom he was given: look at 100 houses before you buy. I failed at this. I looked at maybe 20.

But the logic behind looking at a good number of houses remains. I’m going to take an example from Dan Ariely’s Predictably Irrational (I highly recommend this book). Let’s say you’re out with your agent and you look at two condos, one in a three family home and another in a mid-rise. They both cost about the same and you like them both a lot, but they’re so different and barely have anything in common in terms of community, responsibilities, amenities, and so on. It’ll be really hard to compare and contrast the two. But what if you went and saw a third home, another condo in another 3 family home (maybe it was in worse condition, maybe it was in better condition but in a sketchy neighborhood). All of a sudden, you have something to compare the first 3-family condo to. Ariely found that without something to compare it to, you’ll forget about the mid-rise condo in favor of deciding between the two condos you can compare and contrast. And you’d most likely end up going with the first 3-family condo you saw, after deciding the second was the lacking of the pair. Coming back around, see as many houses as you can so that when you find the house you think is “the one” (which you will, several times), you’ve hopefully seen something to compare it to and can gauge the relative value of the place.

Shopping in Boston/Cambridge mostly happens through open houses. You can set up private showings, but out of the 20 or so properties I looked at, only one was through a private showing. Here’s what normally happens during a week of shopping: at some point throughout the week, either you or your agent will be looking for the new houses being posted online (around Wednesday or Thursday), and your agent will email you the ones that fit your criteria (or you’ll recommend ones to them that you really like). Once condos and houses have been posted, they generally have an open-house that weekend. The most common times I found were between 11am and 2pm.

Let’s say you check out a condo and you really like it. You ask the owner when offers are due and they’ll say something like “Monday at 6pm.” In the 24-36 hours before that time, you’ll contact your mortgage loan agent with the info sheet about the house and say you want to make an offer (at about a 7% markup from the actual listing price, if you have any hope of being competitive). At that point, it’s “Austin’s” job to assess the property, OK you for the amount of money you want to offer for the condo, and write up an offer letter which you include with a bunch of other paperwork your agent will make you sign and send.

According to Bob, most places get between 6 and 15 offers. The first condo I made an offer on had 13, I think. Bob once mentioned one that got 36 offers. As I said before, Demand >>>Supply.

Once you’ve made the offer and the deadline has passed, chances are the listers will go into a bidding war. They’ll come back at you with a “Your offer is really good, but there’s an offer a bit above yours that is waiving both contingencies. We can give you 12 hours to decide if you want to augment your offer.” Or something like that. Or in the case of the first offer I made on a condo, exactly that.

Let me back up and explain about these contingencies. When you submit the offer paperwork to the buyers, there are two contingencies which you either decide to waive and sign, or not sign and keep. The first is the inspection contingency. This is a ‘get out of jail free’ card if the inspection turns up something that would be annoying or pricey to fix, like a roof that needs replacing. If you waive it, you can still have the inspection (and should), but at the point, it only really lets you know about the problem. You can’t back out of the deal because of it. You might try insisting that the sellers fix it before you move in, but if it’s something pricey enough to make you want to bow out, chances are they won’t agree to fix it for you.

The second contingency is the financial contingency. This one says, if for some reason the mortgage lenders decide not to give you the loan after all (because being pre-approved isn’t the same thing as being approved), you’re allowed to back out. Makes complete sense, right? If you need the mortgage in order to buy the place, and the bank won’t give you the mortgage, then you shouldn’t proceed with buying it, right? However, if you waive it, then you’re committed to buying the place whether the bank gives you money to do so or not. Kind of a bad idea to waive if you ask me.

Because the housing market is so competitive in Cambridge, a buyer might waive either or both of these contingencies in order to make their offer more attractive. Waiving both of them means you can do absolutely nothing to get out of the deal if you need to, it’s a guaranteed sale. If you’re a seller, it’s peace of mind that your place is sold. It’s especially attractive if you know that something is wrong with the place (like the roof) and the buyers won’t find out about it until the inspection. At that point, they’ve waived that contingency so they’re stuck with the roof whether they want it or not.

My mom’s pivotal piece of advice to me in this search was, “Agents will always push you to take risky moves if it means closing the deal faster. They just want to get their money.” Bob did advise me that waiving the contingencies could mean winning the bid. However, once I decided that I didn’t want to do that, he was fine with my decision. I didn’t really feel like he was pressuring me to make the riskier decision, but who knows with other agents.

So when I made my offer and they came back with a bidding war asking if I wanted to augment my offer, they meant I should not only up the offer amount enough to match or surpass the other offer, but that I should also drop the contingencies. I upped the offer but didn’t drop the contingencies, and I lost the bid as I knew I would.

You might have to go through this cycle a couple of times before you finally win a bid on a condo. I lucked out on attempt #2. This was a bit of an odd path from start to finish.

Rewind back to the literally the first week I’m starting to look at condos with Bob. He’s sent me a list of everything on the market that fits my bill. There’s one condo that I immediately love–it legit had everything I was looking for– but it disappeared from the listing website in two days. It didn’t even go through an open-house, somebody loved it so much they made an offer right away and the listers took it off the market.

Well, dammit.

I actually end up using this condo as a measuring stick for all the others I’m looking at.

About a month later I mention it again to Bob, so he knows that that condo was the ideal condo for me and can maybe focus his searchers on condos more similar to it. He looked up the listing for the condo and it turns out that it didn’t “sell” exactly, it was just withdrawn from the market. Well, that’s weird.

I asked him to do a bit of digging and it turns out that the original buyers were actually the parents of this girl who was moving to the city to start a job in Kendall Square. She and her best friend were moving to the city together, actually. They saw the listing online and the parents put in an offer right away, since both girls liked it, and the owners accepted the offer. The best friend had a boyfriend, though, and his truck couldn’t fit into the underground parking lot. Also Kendall Square was 2 miles away, which is like, totally too far to, like, bike there and, like, they’d be all sweaty and, like, gross. (Idk if they actually talk like that, but that’s how I imagine they had to talk in order to list those bogus reasons for wanting to back out of the deal). Well, as you know at this point, if your offer is accepted and you want to withdraw from the deal, the only way you can do it is through the inspection or financial contingency. If you back out of the deal without using either of those, you lose your earnest money (like a grand or so that you send with the initial offer to show the buyer that you’re serious).

So, when I asked Bob to ask the listing agent what was going on with the place, they were waiting for the girls to make up their minds about what they wanted to do: either back out and lose money or stick with it. It took about 2 weeks for the girls to make up their minds. Of course, now the owners were probably super bummed because they had to do that listing/open-house/bidding war circus. However, because Bob had been regularly checking the status of that debacle at my request, the listing agent was able to say, “I know someone who’s actually very interested in the condo. Let’s reach out to them.” And that “them” was me. I scheduled a private showing of the apartment and within the week had put in an offer about 5.5% above listing price as a show of good faith. No bidding wars. No competition. It’s like the stars aligned. Like I said, I really lucked out with this condo.

Home Stretch

The hard part of actually having an offer accepted in this market was officially over. Now it’s just a bunch of items on a checklist you need to to. You need to have the inspection done within about 7 days of the offer being accepted. You need to find that attorney. You need to sign the Purchase and Sale Agreement (P&S) (the one where you specify things the current owners should fix before you move in, etc.). You need to send massive amounts of paperwork and documents to the mortgage loan officer so he can find out your deepest dark secrets.

Once you’ve done all that, it’s basically just a waiting game. You’re waiting to hear back from the loan agency that they will be granting you the loan, and then negotiating with them because the interest rate is miserable compared to market standards or something like that.

The time between signing the P&S agreement and actually closing varies with each deal (some need to close fast, like within a month, and some draw it out to two months). At some point during this process, though, you would have committed to a closing date.

Before closing, though, you have a final walk-through of the apartment. Back when you submitted the P&S, you might have asked for a certain number of things to be fixed. For me, it was the closet doors that wouldn’t open and a paint job. The walk-through is the time for you to go through and make sure that these repairs were met to your satisfaction. I’m not sure what you would do in they hadn’t been (maybe a delay in the process?), but if they are, you just proceed to closing as planned.

My closing date was May 15th. This is the day I officially signed my name to an indeterminate number of papers and became a home-owner.

Woo! Here’s to being an adult and having adult responsibilities.

Cheers,

Z